The gold market has a 5,000-year history as a store of value; however, in the last 30 years, the precious metal has established itself as an essential global asset in a world filled with uncertainty, according to the latest report from the World Gold Council.

Tuesday, the WGC celebrated the 30 anniversary of its quarterly and annual Gold Demand Trends report, which looks at all pillars of physical demand in the global marketplace, including jewelry purchases to investor demand and central bank gold holdings.

In an interview with Kitco News, Juan Carlos Artigas, global head of research at the World Gold Council, said that over the last 30 years has evolved to become a more robust and profound market, providing investors around the world with stability and value in their portfolios.

“There is more to gold than one specific market,” he said. “In the last 30 years, the market has changed a lot and the reality is that gold is as important as ever.”

Looking at gold as an asset class, the WGC noted that in the last 30 years, the price had risen from around $330 an ounce, when the first GDT was published, to ending 2022 at $1,814 an ounce.

“With a 5.8% annualized return over the period, gold has outperformed cash, bonds and commodities,” the analysts said. “Gold has also maintained a very low average correlation to stocks, even rising in times of turmoil and performing positively in five out of the past seven recessions, helping investors to reduce their portfolio losses.”

Artigas said that what makes gold a stable and valuable asset is that there is not just one factor that has contributed to gold’s growing role in financial markets.

“If it were just one factor driving gold, that wouldn’t have been sustainable over the last 30 years,” he said.

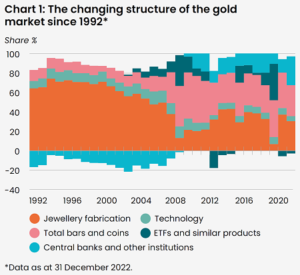

The report noted that in the 1990s, gold was predominantly driven by consumers, with jewelry and technology consumption accounting for the vast majority of gold demand. However, in the last decade fabrication demand now makes up roughly 44% of the total gold market.

Analysts at the WGC noted that jewelry and technology demand are now counterbalances to investment and central bank demand.

“Combined, gold’s role as a consumer good and investment asset underpin its unique dual nature and effective role as a diversifier,” the analysts said.

Gold’s role in financial markets abruptly shifted in 2003 when gold-backed exchange-traded funds were introduced. Investors could now buy gold the same way they could buy stocks.

“This was a significant barrier removed for investors and made it easier for them to buy gold,” said Artigas.

At the same time, two major gold-consuming nations, India and China, saw significant growth in their middle classes, meaning more consumers could buy more gold. The report said that in the 1990s, Asian demand represented about 45% of the global market; today, the region represents about 60%.

Specifically, India and China accounted for less than 20% of total annual demand combined 30 years ago. Today these two countries make up nearly 50%, the report said.

“This is a clear illustration of wealth expansion as one of the most important drivers of gold demand over the long run,” the analysts said in the report.

China has seen the biggest transformation in its domestic gold market as consumers were banned from buying gold up until 2002. China is now the world’s biggest gold-consuming nation and the world’s top gold producer.

“China’s role in today’s global gold market is almost unrecognizable from that of thirty years ago,” the analysts said.

A third transformation in the gold market in the last 30 years has been its renewed role as an important monetary metal. The WGC noted that in the first two decades, central banks were net sellers of the precious metal. The Bank of England is famous for having sold its gold between 1999 and 2002 as prices were trading at historic lows.

The Bank of Canada was another major central bank that sold its gold in the early 2000s.

However, in the last 13 years, central banks have been net buyers. 2022 was a year of insatiable demand, with central banks buying 1,136 tonnes of gold, the highest level of buying since 1967. This was the second highest level of annual demand on record going back to the 1950s, the report said.

Artigas said that central bank demand now represents about 10% of the global market. “And we are not expecting that to go anytime soon,” he said.

“Gold’s performance in times of crisis, its characteristic as a store of value over the long term and its high liquidity were all key reasons for central banks to hold gold,” the analysts said.

As to what the future holds for the gold market in the next 30 years, Artigas said that there is plenty of room for growth; he noted that the massive wealth gap in the world means that any rise in the middle class should create new demand for the precious metal.

He added that emerging markets remain untapped potential for the precious metal.

Artigas also said that evolving technology and the expanding digital marketplace represent new venues for gold.

“There’s plenty of ways in which the gold market can grow,” he said. “There are real and growing applications for gold in the technology sector. There are a lot of things to be excited about regarding gold’s future.”

Source: Kitco